Understanding Construction Loans & Financing Options

Building a home from the ground up is exciting, but it also brings one big question: how will you pay for it? That’s where construction loans and related financing options come in. Unlike a standard 30-year mortgage you use to buy an existing house, construction loans are short-term, highly customized, and tied to the progress of your build.

In the U.S. housing market, construction costs have climbed to record levels as a share of new-home prices, and interest rates remain higher than pre-2020 norms. That makes understanding construction loans more important than ever if you’re planning to build or undertake major renovations.

This guide walks you through what construction loans are, how they work, the main types, qualification rules, current rate and cost trends, and where this market is headed over the next few years.

Along the way, you’ll see how construction loans compare to other financing options and get practical tips to improve your approval odds and keep your project on budget.

Whether you’re a first-time homebuilder or an experienced real-estate investor, understanding construction loans will help you turn a set of plans into a finished home without nasty financial surprises.

What Are Construction Loans and How Do They Work?

Construction loans are short-term loans that finance the cost of building or significantly renovating a home. Instead of giving you all the money upfront, the lender disburses funds in stages—called draws—as work is completed and inspected.

In a typical scenario, a construction loan:

- Covers land, labor, and materials, and often permits and certain soft costs.

- Has a term of about 12–18 months, long enough to complete most residential builds.

- Is usually interest-only during construction, based on the amount that has been drawn rather than the full approved balance.

- Requires a detailed budget, schedule, and architectural plans, because the lender is taking on more uncertainty than with a standard mortgage.

Here’s the basic flow of most construction loans:

- Approval – You and your builder submit plans, specs, costs, and your personal financial information.

- Closing – You sign the construction loan (and sometimes the permanent mortgage at the same time).

- Draws & Inspections – The builder completes work in phases (foundation, framing, rough-in, finishing). After each phase, the lender orders an inspection and, if everything checks out, releases a draw to pay the builder.

- Interest-Only Payments – You typically pay only interest on the drawn balance during construction, helping manage cash flow while you may still be paying rent or another mortgage.

- Conversion or Payoff – At the end of the build, either the construction loan converts into a standard mortgage (construction-to-permanent loan) or you pay it off with a new mortgage (construction-only loan).

Because construction loans are not secured by a finished home at the outset, lenders treat them as higher risk. That usually means stricter underwriting, higher down payments, and slightly higher interest rates than a conventional purchase mortgage.

However, they may also offer powerful flexibility, including contingency reserves for cost overruns and interest reserves that cover your construction-phase payments.

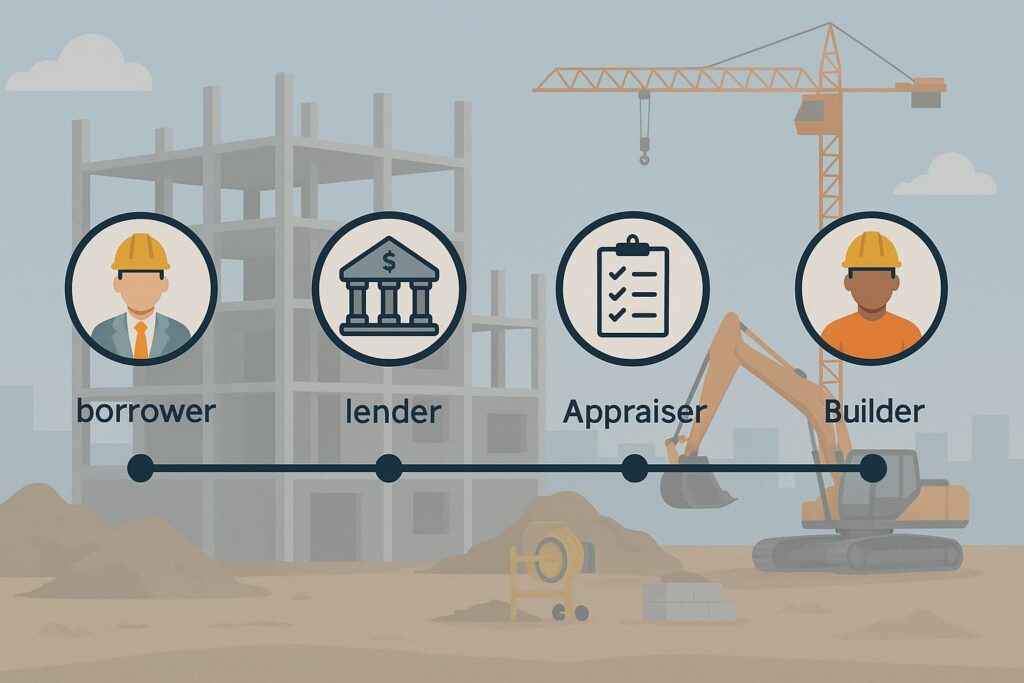

Key Parties and Timeline in a Construction Loan

Understanding construction loans also means understanding who is involved and how the timeline typically unfolds.

The key parties are:

- Borrower (You) – Provides income documentation, credit history, and down payment. You’re responsible for payments on the construction loan and the permanent mortgage.

- Builder/General Contractor – Must usually be licensed, insured, and experienced, often vetted or approved by the lender. Many lenders will not approve owner-builder construction loans unless you can show professional building experience.

- Lender – Underwrites both your financial strength and the project’s feasibility. The lender manages the draw schedule, inspections, and conversion to permanent financing.

- Appraiser – Estimates the as-completed value of the home based on plans, specs, and comparable properties. This value helps determine the maximum size of your construction loan.

A common timeline for construction loans looks like this:

- Pre-approval (1–4 weeks) – You explore construction loans and financing options with lenders, get pre-qualified, and confirm how much budget you can realistically support.

- Design & Bid Phase (1–3 months) – You finalize plans with an architect and builder, gather bids, and refine your construction cost estimates and schedule.

- Full Application & Underwriting (3–8 weeks) – The lender reviews your credit, income, assets, plans, and builder qualifications. They order an appraisal, and you may negotiate final loan terms.

- Closing & Groundbreaking – You close on the construction loan (and possibly the permanent mortgage). The builder breaks ground and begins the draw schedule.

- Construction (6–18+ months) – Draws are requested at milestones; the lender inspects and releases funds. You make interest-only payments on the drawn balance.

- Completion & Conversion – Once the home is finished and has a final inspection and often a certificate of occupancy, the construction loan is either converted to a permanent mortgage or paid off with a separate end loan.

Planning your timeline carefully is critical, because construction delays can extend the interest-only period and increase total cost. Many borrowers build in a contingency both in the construction loan and in their calendar to handle the unexpected.

Types of Construction Loans Available in the U.S.

There isn’t just one type of construction loan. Instead, U.S. borrowers can choose from several construction loans and financing options, each with different pros and cons. Picking the right structure can save you money and reduce risk.

At a high level, the main types of construction loans are:

- Construction-to-Permanent (Single-Close) Loans

- Construction-Only (Two-Close) Loans

- Renovation or Rehab Construction Loans

- Government-Backed Construction Loans (FHA, VA, USDA)

- Lot and Land Loans (often used alongside construction loans)

All of these are still construction loans in the sense that they fund a build or major renovation, but their structure and long-term impact on your finances differ significantly.

Construction-to-Permanent (One-Time Close) Loans

A construction-to-permanent loan, also called a single-closing or one-time close loan, combines the construction loan and the permanent mortgage into a single package with one closing.

Here’s how these construction loans usually work:

- You apply once, and the lender underwrites both the construction phase and the long-term mortgage up front.

- During construction, the loan functions as a short-term, interest-only construction loan, with draws released as work is completed.

- When the home is finished, the loan automatically converts to a standard mortgage (fixed-rate or adjustable) for 15, 20, or 30 years, depending on your terms.

- You avoid a second closing, additional closing costs, and the risk that your financial situation changes and you can’t qualify for a new mortgage at the end of construction.

Government-backed programs also offer one-time close construction loans. For example, the FHA One-Time Close program lets you finance land, construction, and the permanent mortgage in a single 3.5%-down loan (subject to FHA limits), making construction loans more accessible to borrowers with modest down payments.

Advantages of construction-to-permanent loans:

- Simplicity – One application and one closing.

- Rate protection – Often allows you to lock in your long-term rate up front, which is valuable in a rising-rate environment.

- Lower closing costs overall than two separate loans.

Potential drawbacks:

- Less flexibility if you want to shop for better mortgage terms at the end of construction.

- Some lenders may have stricter requirements since they’re committing to long-term financing from day one.

Construction-Only (Two-Time Close) Loans

A construction-only loan (or two-time close) is a short-term loan that finances the build, but does not automatically convert to a mortgage. When the home is complete, you must refinance into a permanent loan to pay off the construction balance.

How these construction loans typically work:

- You close first on the construction loan.

- You make interest-only payments during construction, with funds released in draws as usual.

- Once the home is finished, you apply for a separate mortgage (conventional, FHA, VA, etc.).

- You pay a second set of closing costs, and your new rate is based on market conditions at that time.

Advantages:

- Flexibility to shop around for the best permanent mortgage after construction, when your income, credit, or rate environment may have changed.

- Potentially easier to switch lenders or products if something about your situation shifts during the build.

Disadvantages:

- Two sets of closing costs and underwriting.

- Rate risk – if rates rise significantly during construction, your long-term payments may be higher than expected.

- If your financial situation worsens, you could struggle to qualify for the permanent loan, creating serious stress.

Construction-only loans may make sense if you’re very confident about your long-term borrowing strength and believe rates could fall by the time your home is complete.

Renovation and Home Improvement Construction Loans

You don’t need to be building a brand-new house to use construction loans. If you’re doing a major renovation or gut rehab, you might need a renovation construction loan or a rehab loan.

These construction loans are designed to finance large projects such as:

- Adding a second story or major addition.

- Completely rebuilding a home’s interior while keeping the shell.

- Converting a multi-unit property or reconfiguring the layout.

Some programs, such as Fannie Mae’s HomeStyle or FHA 203(k), roll both purchase and renovation costs into a single loan. Others act more like a traditional construction loan, releasing funds in draws based on progress.

Compared with simple home-equity loans or HELOCs, renovation construction loans:

- Rely on the after-renovation value (ARV) of the property to determine how much you can borrow.

- Require a detailed scope of work, budget, and contractor bids.

- Often include more inspections and oversight, similar to new-build construction loans.

These products are especially valuable in high-cost markets where existing homes need major updating, or in neighborhoods where buying and rehabbing is more cost-effective than building or buying new.

Government-Backed Construction Loans (FHA, VA, USDA)

For eligible borrowers, government-backed construction loans can dramatically reduce down-payment requirements and broaden access to construction financing options.

Key programs include:

- FHA One-Time Close Construction Loans – Allow as little as 3.5% down, with flexible credit guidelines, combining land, construction, and permanent mortgage into a single loan.

- VA Construction Loans – Designed for eligible veterans and service members. Some lenders offer VA construction-to-perm loans with low or even zero down, but availability can be more limited than standard VA purchase loans. (Specific terms vary by lender, so you must shop around.)

- USDA Construction Loans – Targeted at rural and suburban areas that meet USDA eligibility. They can offer low or zero down payments and competitive rates, but the property must be in a qualifying location and meet program standards.

Government-backed construction loans can be an excellent fit if:

- You have strong income but a smaller down payment.

- You’re a first-time homebuyer who wants to build rather than buy.

- You’re a veteran or buying in a rural area.

The trade-off is that these loans often involve more paperwork and stricter property guidelines, including inspections, appraisal standards, and limits on certain property types.

Current Market Conditions, Costs, and Interest Rates for Construction Loans

If you’re evaluating construction loans today, you must understand where costs and interest rates stand in the current U.S. market.

According to the National Association of Home Builders’ Cost of Construction Survey, construction costs now make up about 64.4% of the sales price of a typical new single-family home, a record high and a notable increase from 60.8% in 2022.

Data from recent studies shows that in 2024:

- The average finished sales price of a new single-family home was around $665,000, with total construction costs close to $428,000, and costs rising faster than overall prices.

- Rising prices for materials and labor, along with tariffs on key inputs like lumber, steel, and other materials, have further increased build costs by several thousand dollars per home.

On the financing side, construction loans typically carry higher interest rates than standard mortgages because they are shorter-term and riskier for lenders. Recent industry data for 2024–2025 suggests that:

- Construction loan rates often range roughly from 4% to 12%, depending on the lender, borrower profile, and project risk.

- Meanwhile, 30-year fixed mortgage rates have hovered around the high-6% range at various points in 2025, according to housing market reports, influencing what you might pay once your construction loan converts to a permanent mortgage.

In addition to higher costs and rates, builders and lenders are navigating:

- Tariffs and trade policy changes that impact materials prices.

- Labor shortages in construction trades, which can extend timelines and increase bids.

- Tighter lending standards in some areas, especially for speculative construction or investment projects.

All of this means that when you explore construction loans and financing options in 2025, you should:

- Add healthy contingencies (often 10–15% or more) to your construction budget.

- Be realistic about timeline risks, especially in markets with labor or permitting backlogs.

- Understand that your construction loan rate may be significantly higher than the permanent rate you eventually lock.

How Rising Construction Costs Affect Your Budget

Rising construction costs directly influence how much you need to borrow and how far your money will go. Because construction loans are based on either the total cost of construction or a percentage of the finished appraised value, higher costs can affect:

- Loan Size – If costs rise but the appraised value doesn’t keep up, you may need to bring more cash to closing to stay within loan-to-value (LTV) limits.

- Down Payment – Lenders often require 20–30% down on construction loans. As total project costs rise, so does the dollar amount of that down payment.

- Debt-to-Income (DTI) Ratios – Higher loan balances and potentially higher rates can push your monthly payment upward, making it harder to stay under common DTI caps (often around 43–45% for many lenders).

Additionally, rising costs can create a gap between original bids and actual invoices as the project progresses. That’s why many smart borrowers:

- Build in contingency reserves within the construction loan (the lender sets aside extra funds that can be tapped if certain costs increase).

- Negotiate guaranteed maximum price (GMP) contracts with builders to cap cost overruns, where possible.

- Consider design choices and materials that are less sensitive to volatile commodities pricing.

Looking ahead, industry forecasts and international cost-tracking bodies suggest that construction costs are likely to keep trending upward through 2030 due to structural labor constraints and ongoing materials inflation, even if the pace of increases fluctuates year to year.

Eligibility Requirements for Construction Loans

Because construction loans pose more risk to lenders, qualification standards are often more demanding than for standard mortgages. If you want the best terms on construction loans and financing options, it helps to know what lenders are looking for before you apply.

Key eligibility factors include:

- Credit Score – Many lenders prefer 680+ for conventional construction loans, although some government-backed programs like FHA may accept lower scores.

- Debt-to-Income Ratio (DTI) – Lenders typically want your DTI to be 45% or lower, including the new construction loan payment.

- Down Payment – Conventional construction loans commonly require 20–25% down, sometimes more for complex or speculative builds. FHA construction loans can go as low as 3.5% down, subject to loan limits and other criteria.

- Income & Employment – Stable, documentable income (W-2, tax returns, 1099s) is crucial. Self-employed borrowers may need to provide additional documentation, such as several years of tax returns.

- Reserves – Some lenders want to see cash reserves sufficient to cover several months of payments and unexpected costs, especially given the unpredictability of construction timelines.

On the project side, lenders will also scrutinize:

- Builder Qualifications – Most lenders require a licensed, insured, and experienced general contractor. They may ask for references, a portfolio, and proof of good standing with local and state authorities.

- Plans and Specs – Detailed architectural drawings, engineering plans (if needed), and a line-item budget that includes labor, materials, permits, and fees.

- Appraised Value – An appraiser will use the plans and comps to estimate the as-completed value. This value helps determine your maximum loan amount and required down payment.

To improve your chances of approval for construction loans:

- Work on raising your credit score before you apply—pay down revolving debt, correct errors, and avoid opening new accounts.

- Lower your DTI by paying off smaller loans or consolidating high-interest debt.

- Accumulate a strong cash cushion, as lenders are more comfortable when they see you have reserves beyond your minimum down payment.

- Choose a reputable builder who has experience with projects similar to yours and is comfortable working within a lender’s draw and inspection framework.

Step-by-Step: How to Apply for a Construction Loan

Because construction loans involve both you and your builder, the application process can feel more complex than a typical mortgage. Breaking it down into steps makes it manageable.

1. Set Your Budget and Goals

Before speaking to lenders, clarify your total budget, including land, construction, contingency, closing costs, and furnishings. Use realistic estimates and consider consulting both a builder and a financial advisor.

2. Choose a Builder and Finalize Plans

Construction loans depend on solid plans. Work with a builder or design-build firm to create:

- Preliminary and then final architectural plans.

- A detailed scope of work and specifications (finishes, materials, systems).

- A line-item cost breakdown with realistic allowances.

3. Shop for Lenders and Get Pre-Qualified

Talk to multiple lenders that actively originate construction loans, such as large banks, regional lenders, credit unions, or specialized mortgage companies. Ask about:

- Types of construction loans offered (construction-to-perm, construction-only, FHA, VA, USDA).

- Required down payments, rate structure, and fees.

- Builder approval requirements and draw procedures.

4. Submit a Full Application

Your construction loan application will typically require:

- Personal financials: W-2s, tax returns, pay stubs, bank statements, list of debts.

- Project documents: plans, specs, budget, builder contract, and schedule.

- Information about the land (purchase contract or deed if you already own it).

The lender orders an appraisal based on the as-completed home and may require additional inspections or feasibility checks.

5. Underwriting and Conditional Approval

An underwriter reviews your profile and the project. They may issue conditions, such as:

- Updated income documents.

- Clarifications on budget items.

- Revisions to the draw schedule.

You may negotiate terms or adjust your project scope to fit the lender’s requirements.

6. Closing the Construction Loan

Once conditions are cleared, you sign the construction loan documents. For construction-to-perm loans, this may also include your permanent note and mortgage. You’ll pay closing costs and fund your down payment at this stage.

7. Draws, Inspections, and Project Management

As the build progresses, the builder requests draws according to the agreed schedule (e.g., after foundation, framing, mechanical rough-ins, drywall, and final finishes). The lender sends an inspector to verify that the work is completed, then releases funds directly to the builder or title company.

Your responsibilities during this phase include:

- Monitoring change orders closely.

- Keeping an eye on draws to ensure they match progress.

- Making interest-only payments on the drawn balance.

8. Completion, Final Inspection, and Conversion

Once the home is finished, you obtain a certificate of occupancy and the lender conducts a final inspection. With construction-to-permanent loans, your loan transitions into a long-term mortgage. With construction-only loans, you refinance into the permanent loan product of your choice.

Comparing Construction Loans to Other Financing Options

Construction loans are powerful tools, but they aren’t the only way to finance a build or major renovation. Understanding how construction loans compared to other options can help you pick the right structure.

Construction Loans vs. Traditional Mortgages

- A traditional mortgage is used to buy an existing home; funds are disbursed once at closing.

- Construction loans disburse funds in stages and are meant for properties that aren’t yet built or fully habitable.

- Construction loans usually have short terms, interest-only payments, higher rates, and more inspections.

- With a construction-to-perm structure, you eventually end up with a standard mortgage, but you must first navigate the construction phase.

Construction Loans vs. Home Equity Loans / HELOCs

If you already own a home with significant equity, you might tap that equity to fund construction or renovation:

- Home Equity Loan – Lump-sum second mortgage with a fixed rate and fixed payment.

- HELOC – Revolving line of credit secured by your home, with variable rates and flexible draws.

Compared with construction loans:

- Home equity products typically have simpler underwriting and fewer inspections.

- They’re most useful for smaller projects or when you have enough equity to cover the entire build or renovation.

- They may not provide enough financing for ground-up construction, especially if you need to buy land.

Construction Loans vs. Personal Loans and Credit Cards

For small projects, some homeowners consider unsecured personal loans or even credit cards. While these can work for minor improvements, they are rarely suitable for full construction due to:

- Much higher interest rates than construction loans.

- Lower maximum amounts.

- Shorter terms, which can strain cash flow.

Construction Loans vs. Builder Financing

Some builders offer in-house financing or preferred lenders for construction loans and end mortgages. The benefits can include:

- Streamlined process and familiarity with the builder’s workflow.

- Possible incentives like rate buydowns or closing-cost credits.

However, you should still compare these construction loans with quotes from independent lenders to ensure you’re truly getting the best combination of rate, fees, and flexibility.

Future Trends in Construction Loans and Homebuilding Finance

If you’re starting a multi-year building journey, it’s smart to consider where construction loans and homebuilding finance are heading. While no one can predict the future perfectly, several trends are emerging:

- Digitization of Construction Loans

Lenders are investing heavily in online applications, digital draw management, and e-closings. In the coming years, expect:

- Faster approvals using automated income and asset verification.

- Real-time draw requests and status tracking via mobile apps.

- Better integration among builder, lender, and title company.

- Faster approvals using automated income and asset verification.

- Continued Upward Pressure on Construction Costs

Industry surveys and forecasts suggest that construction costs will likely continue rising through 2030, driven by labor shortages, higher wages, and materials inflation.

International data from cost-consulting bodies projects double-digit increases in building costs over the decade, and U.S. data already shows record-high cost shares in new-home prices. - Environmental and Energy-Efficiency Incentives

Expect construction loans to increasingly factor in green building techniques, energy-efficient systems, and resilient design. Over time, we’re likely to see:

- More lenders offering rate discounts or flexible terms for homes that meet certain energy standards.

- Better integration of solar, battery storage, and EV infrastructure into build budgets and appraisals.

- More lenders offering rate discounts or flexible terms for homes that meet certain energy standards.

- Modular and Off-Site Construction

Modular and panelized construction can shorten build times and potentially reduce cost overruns. As these methods gain traction, lenders may adapt construction loans to:

- Adjust draw schedules for factory-based production.

- Streamline inspections tailored to off-site and on-site phases.

- Adjust draw schedules for factory-based production.

- Policy and Regulatory Shifts

Federal housing agencies regularly adjust conforming loan limits and program guidelines, affecting how easily construction loans can be converted into agency-backed mortgages. Recent increases in conforming loan limits reflect rising home prices and could support somewhat larger construction-to-perm loans in the future.

For borrowers, the implication is clear: construction loans are likely to become more digital, more tightly connected to sustainability goals, and continually shaped by cost pressures and policy changes. Building flexibility into your financing plan—and working with lenders that specialize in construction loans—will help you adapt as the market evolves.

Tips to Make Construction Loans Work for You

Because construction loans involve more moving parts than a standard mortgage, thoughtful planning can significantly reduce stress and cost.

1. Choose the Right Structure (Single-Close vs. Two-Close)

If you value simplicity and want to lock in your mortgage rate early, a construction-to-permanent loan is often ideal. If you believe rates may fall or you want to shop aggressively for permanent financing later, a construction-only loan can provide flexibility—just remember the extra closing costs and rate risk.

2. Add Contingencies to Your Budget

Given modern cost volatility, many experts recommend at least 10–15% contingency in your construction budget. Some construction loans allow a built-in contingency line item. If you don’t use it, it can simply be applied to principal reduction.

3. Lock Your Construction Loan and Permanent Rate Strategically

Ask lenders:

- Whether you can lock both construction and permanent rates at application.

- If there is a float-down option should rates improve before conversion.

Understanding these details can save thousands over the life of your loan, especially in a rising-rate environment.

4. Scrutinize the Draw Schedule

A well-designed draw schedule should:

- Align with real milestones and cash needs.

- Incentivize the builder to stay on schedule.

- Avoid front-loading funds in a way that leaves the lender—and you—exposed if the builder walks away.

5. Protect Yourself Legally and Financially

- Use clear written contracts with your builder, specifying timelines, change-order procedures, and responsibility for delays.

- Consider hiring an independent construction manager or inspector in addition to the lender’s inspector, especially for complex projects.

- Make sure you understand lien waivers and how subcontractors get paid to avoid future title problems.

6. Keep Your Financial Profile Stable During Construction

- Avoid taking on new large debts (cars, personal loans) while your construction loans are active.

- Maintain or increase your cash reserves in case of delays.

- Monitor your credit, as the lender may re-check it before converting the loan to permanent status.

By managing these elements carefully, construction loans become a powerful tool rather than a source of stress—helping you complete your home on time and within budget.

FAQs

Q.1: What credit score do I need for a construction loan?

Answer: Minimum credit scores vary by lender and by type of construction loan, but stronger credit is usually required than for a standard mortgage. Many conventional lenders look for scores around 680 or higher for construction loans, especially if you’re building a custom home or using a construction-only structure.

Government-backed programs, such as FHA One-Time Close construction loans, may allow scores in the low- to mid-600s, though lenders can set higher overlays.

Beyond the raw score, lenders focus heavily on your broader risk profile. They assess your debt-to-income ratio, employment stability, reserves, and past payment history.

Even with a high credit score, a very tight DTI or limited savings can lead to stricter terms or smaller approved loan amounts. Conversely, an applicant with a slightly lower score but excellent income and strong reserves might still qualify for competitive construction loans and financing options.

You can boost your chances of approval and better terms by working on your credit profile 3–12 months before you apply. Pay down revolving credit, avoid late payments, and limit new credit inquiries.

If your score is just below a key threshold (for example, 679 when the lender prefers 680), minor improvements can yield meaningful benefits in rate and fees. Because construction loans involve more risk and complexity, every bit of extra credit strength helps.

Q.2: How much down payment is required for construction loans?

Answer: For conventional construction loans, many U.S. lenders require 20–25% down, and some may ask for more if the project is complex, speculative, or in a volatile market. That down payment is usually calculated as a percentage of either the total project cost (land plus construction) or the as-completed appraised value, whichever is lower.

Government-backed construction loans can significantly reduce this requirement. FHA construction-to-permanent loans may allow down payments as low as 3.5%, subject to FHA loan limits and standard guidelines.

VA and USDA construction loans, when offered, can sometimes support very low or even zero down payments for eligible borrowers and qualifying locations.

Remember that your equity in the land counts toward the down payment. If you already own the lot and have paid it down—or if its value has appreciated—that equity can reduce the amount of new cash you need to bring to closing.

If you bought the land recently, lenders may base the value on either the purchase price or the current appraised value, depending on their guidelines. Always ask how your lender treats land equity in construction loans and financing options so you can plan accurately.

Q.3: Are construction loans more expensive than regular mortgages?

Answer: Generally, yes—construction loans tend to be more expensive than standard purchase mortgages, especially during the construction phase. There are several reasons for this. First, they’re short-term, customized loans secured by a property that doesn’t yet exist, which adds risk for the lender.

Because of this, interest rates on construction loans are usually higher than on long-term fixed mortgages and may be tied to a variable benchmark plus a margin. Recent data shows construction loan rates often spanning 4% to 12%, depending on borrower and project risk.

Second, construction loans come with additional fees, such as inspection fees, draw fees, and sometimes higher origination charges. Each draw may involve administrative work and an on-site inspection before funds are released. That extra oversight protects both you and the lender but does add cost.

However, once construction is complete and you either convert to a permanent mortgage or refinance, your long-term rate can look very similar to any other mortgage, especially if the loan is sold to or backed by agencies like Fannie Mae or FHA.

The key is to look at the total cost of the project: interest paid during construction, all fees, and the ultimate permanent mortgage rate. In many cases, construction loans are still the most efficient way to fund a building, as long as you structure them wisely and shop lenders carefully.

Q.4: Can I be my own general contractor for a construction loan?

Answer: Some borrowers hope to save money by acting as their own general contractor (GC). While this is sometimes possible, many lenders are hesitant to approve owner-builder construction loans unless you can demonstrate substantial professional building experience and a strong track record.

From a lender’s perspective, inexperienced project management increases the risk of cost overruns, delays, and quality problems that can affect the value of the collateral.

If a lender does allow an owner-builder structure, expect stricter conditions. These could include higher down payments, more frequent inspections, and tighter draw controls. You’ll need to supply detailed schedules, subcontractor bids, and proof that you understand permitting, code requirements, and local building practices.

For most borrowers, lenders strongly prefer or require that construction loans be tied to a licensed, insured, and vetted contractor. That doesn’t mean you can’t be deeply involved in design, budgeting, and selections.

But letting a professional GC handle day-to-day management and coordination usually results in smoother draws, fewer surprises, and better alignment with lender expectations. If your main goal is cost savings, consider negotiating with reputable builders on margins, design choices, and materials rather than going fully owner-builder with your construction loans.

Conclusion

Construction loans can feel intimidating at first, but they’re simply specialized tools designed to handle the complexity of building or heavily renovating a home.

When you break them down, most construction loans follow a predictable pattern: detailed up-front planning, supervised draws during the build, and a transition to a permanent mortgage once the home is complete.

If you’re dreaming of a custom home, a major addition, or a full-scale renovation, taking the time to understand construction loans and financing options can pay off for years to come.

You’ll make smarter decisions about whether to choose construction-to-permanent or construction-only, when to lock rates, how much contingency to build into your budget, and which lender and builder are the best fit.

In today’s U.S. market—where construction costs are high, interest rates remain elevated compared with the last decade, and materials and labor face ongoing pressures—it’s more important than ever to approach construction loans with a clear strategy and realistic expectations.

If you do, these loans become less of a hurdle and more of a bridge between your vision and the finished home you’ll live in.

Before you break ground, consider speaking with multiple lenders, a knowledgeable builder, and possibly a financial planner.

Together, they can help you align your construction loans and financing options with your long-term goals, whether that’s building your forever home, creating investment property, or designing a space that grows with your family.